By Sam Walker of SamWalkerOBXNews.com

Businesses in North Carolina that add a credit card processing fee to customer bills are reminded that they have to pay sales tax on the surcharge.

N.C. Restaurant and Lodging Association President & CEO Lynn Minges said in an email the state Department of Revenue has been conducting audits that found a number of merchants have failed to catch the oversight.

“If you currently impose a surcharge for credit card purchases, we encourage you to check your Point-of-Sale Systems to confirm that this is your current practice,” Minges said.

The NCRLA is the largest advocate of hospitality-related businesses statewide.

The sector has more than 20,000 businesses statewide, employs 9% of the state’s workforce and generates more than $34.9 billion in sales annually.

Minges noted that the email was not to be considered legal advice from the NCRLA, and that business owners should consult a licensed attorney to address specific questions.

Since the COVID-19 pandemic started, the use of cards skyrocketed to around 90% of all transactions.

Card processing companies have since raised the fees they charge merchants to as much as 3.5% per transaction.

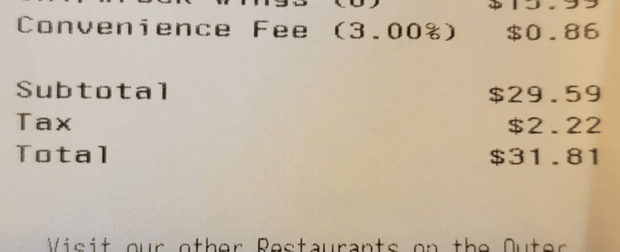

To overcome the increase in their bottom line, merchants started passing along the fee to customers who use cards using the words “convenience fee”, “processing fees” and other terms.

At the same time, many started offering cash customers discounts that matched the amount of the fee.

A bill that had bipartisan support was introduced in the state House in February 2023 to outlaw the practice, but no action was taken on the proposal.

A bulletin issued earlier this year by the Department of Revenue details the requirements of merchants to charge sales tax on the transaction fee if they pass it on to customers.

“Surcharges made by a retailer for a retail sale, whether separately stated or not, are part of the sales price of an item subject to sales and use tax. (Examples: Fees for using a credit card, fuel surcharges, trip surcharges, service fees unless exempt under SUTB 32-18, etc.”

Minges also shared an example from a certified public accountant of an audit conducted of a restaurant for sales tax compliance for the last three years beginning in June 2021, and that the establishment had been fully reporting all sales and paid tax correctly.

“However, in June 2022 this establishment began to charge their customers a 3% fee to reimburse them for the fees on Credit Card purchases – a practice that has become common in the hospitality and retail industries,” Minges said.

“This was set up in their Point-of-Sale (POS) system by the firm hired to provide those support services,” Minges said. “That charge was set in the POS system to be free of sales tax. Commonly called in the POS system, ‘Non-Cash Adjustment’ or sometimes simply “Service Charge’.”

While the state auditor said the charge had to be taxed at the correct rate, 7% in the case of the business that was audited, their POS system was not charging it because it could not be programmed to do so correctly.

North Carolina law is very specific about how sales tax is to be applied, and that the seller is not able to deduct any of their costs from the base.

“Some states make exceptions for things like shipping,” Minges said.”

NCGS §105-164.3.(237) provides the following on sales price:

The total amount or consideration for which an item is sold, leased, or rented. The consideration may be in the form of cash, credit, property, or services. The sales price must be valued in money, regardless of whether it is received in money.

The term includes all of the following:

- The retailer’s cost of the item sold.

- The cost of materials used, labor or service costs, interest, losses, all costs of transportation to the retailer, all taxes imposed on the retailer, and any other expense of the retailer.

- Charges by the retailer for any services necessary to complete the sale.

- Delivery charges.

- Installation charges.

- Repealed by Session Laws 2007-244, s. 1, effective October 1, 2007.

- Credit for trade-in. The amount of any credit for trade-in is not a reduction of the sales price.

- The amount of any discounts that are reimbursable by a third party and can be determined at the time of sale through any of the following: I. Presentation by the consumer of a coupon or other documentation. II. Identification of the consumer as a member of a group eligible for a discount. III. The invoice the retailer gives the consumer.

The term does not include any of the following:

- Discounts that are not reimbursable by a third party, are allowed by the retailer, and are taken by a consumer on a sale.

- Interest, financing, and carrying charges from credit extended on the sale, if the amount is separately stated on the invoice, bill of sale, or a similar document given to the consumer.

- Any taxes imposed directly on the consumer that are separately stated on the invoice, bill of sale, or similar document given to the consumer.

In her email, Minges also shared an interpretation provided by the N.C. Department of Revenue, “essentially saying that while the credit card expense is a direct result of how the customer chose to pay, it is still an expense of the business.”

“As such, it is considered part of the selling price even if it is itemized,” Minges said of the interpretation. “Further, it would be considered part of the selling price whether it is passed through at cost or marked up.”

“As part of the selling price, it will be taxed in the same manner as the underlying transaction,” Minges said. “If the product being sold is taxable, the fee is taxable, if the product being sold is nontaxable, the fee is nontaxable.

Minges said the NCRLA is meeting with colleagues at the N.C. Association of CPAs, the N.C. Retail Merchants Association, and other industry stakeholders about the interpretation, and possibly seeking action by the N.C. General Assembly.

“(They are) discussing the potential desire for a legislative clarification with the argument that this charge is simply a reimbursement by the consumer for charges incurred on their behalf by the merchant rather than a payment for goods or services,” Minges said.

“In the meantime, our guidance is to follow the interpretation from the NC Department of Revenue to avoid the potential of having to pay the tax out-of-pocket through an audit,” Minges said.